COLOMBO – The latest analysis of local banks suggests that Sri Lanka’s banking sector may be far stronger than headline profit figures indicate, once the accounting effects of sovereign debt restructuring are stripped away.

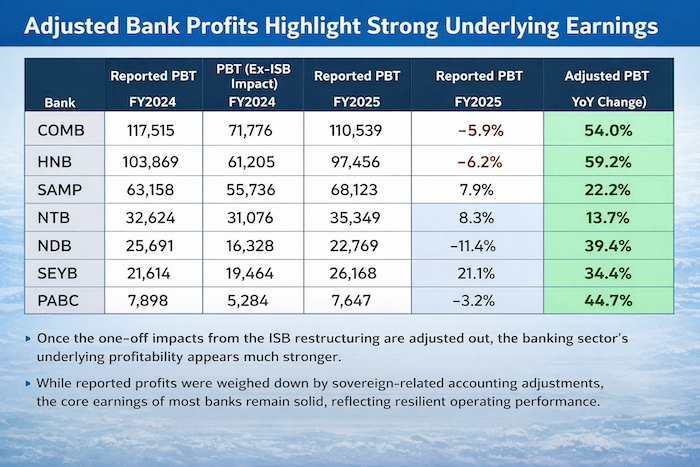

On the surface, reported profits for several major banks appear weak. According to the figures, leading institutions such as Commercial Bank of Ceylon and Hatton National Bank recorded year-on-year profit declines of 5.9 percent and 6.2 percent respectively.

But analysts say those numbers are misleading.

The apparent decline stems largely from accounting adjustments linked to the restructuring of Sri Lanka’s International Sovereign Bonds (ISBs) during the country’s financial crisis. When those one-off impacts are removed, the underlying profitability of the sector looks markedly stronger.

Analyst’s adjusted figures show Commercial Bank’s core earnings rising by 54 percent, while Hatton National Bank posted a remarkable 59.2 percent increase in underlying profit.

Other banks also show robust gains once the ISB impact is excluded. Sampath Bankrecorded adjusted profit growth of 22.2 percent, while Nations Trust Bank showed a 13.7 percent improvement. Meanwhile National Development Bank PLC and Seylan Bankreported adjusted growth rates of 39.4 percent and 34.4 percent respectively.

Pan Asia Banking Corporation, which appeared to show a slight profit decline on the surface, recorded an adjusted increase of nearly 45 percent.

Market observers say the data points to a banking sector that has weathered the worst of the sovereign crisis and is now demonstrating solid operating resilience.

Be that as it may, the Colombo Stock Exchange has yet to fully reflect this recovery in bank share valuations.

If the underlying earnings momentum continues, analysts believe investors may soon begin reassessing whether Sri Lanka’s banking sector is still being priced for a crisis that has largely passed.

WHY SOVEREIGN DEBT RESTRUCTURING HITS BANK PROFITS

When a government restructures its sovereign debt, the impact does not remain confined to the Treasury. It quickly spreads into the balance sheets of the country’s banking system.

The reason is simple. Banks are among the largest holders of government securities, including Treasury Bills, Treasury Bonds and other sovereign-linked instruments. These assets are normally considered safe and form a core part of a bank’s investment portfolio.

When Sri Lanka undertook its sovereign debt restructuring following the financial crisis, the terms of many government securities were altered. Interest rates were reduced, repayment periods were extended and the economic value of some instruments effectively declined.

Under international accounting rules, banks must then revalue those assets immediately, recognising the reduced value as a loss or adjustment in their financial statements. This does not necessarily mean banks have lost cash or that the loans have disappeared. Rather, it reflects the fact that the bonds they hold are now worth less than originally expected.

These adjustments can temporarily depress reported profits, even if the bank’s underlying operations remain strong. Lending activity, deposit growth and fee-based income may continue to perform well, but the accounting impact of the sovereign restructuring still appears in the annual results.

That is why analysts often examine “adjusted profits” that exclude these one-off restructuring effects. When those adjustments are removed, the core earnings performance of the banking sector can appear significantly stronger than the headline figures suggest.

In short, sovereign debt restructuring does not only reshape government finances. It also temporarily reshapes how bank profitability is reported.

Adjusted profit does not mean the loss disappeared.The bank still lost value on the bonds.But the adjustment helps investors see that:

• the loss is a one-time restructuring event

• not a permanent weakness in the bank’s core business.