Fitch Ratings – Asia-Pacific sovereign credit profiles face heightened downside risks from a prolonged Iran conflict, as the region’s heavy reliance on imported oil and gas raises exposure to higher prices and potential supply disruptions, Fitch Ratings says.

Large shares of the oil and gas products used in the region pass through the Strait of Hormuz, and disruptions could also affect related inputs, such as fertilizers and petrochemical feedstocks. The result would be a negative terms-of-trade shock for most sovereigns, with knock-on effects for inflation, growth, and the public finance outlook.

Energy prices are the most direct transmission channel. Fitch’s baseline assumes Brent stays near current levels through March, then eases to average USD 70/bbl in 2026. In an adverse three-month conflict scenario, with oil prices rising to an average of USD 128/bbl in 2Q26 and USD 100/bbl for 2026 as a whole, some APAC sovereigns, particularly in South and Southeast Asia, could face negative rating pressure, depending on their fiscal and external buffers and the authorities’ policy responses. APAC sovereigns’ exposure is amplified by high dependence on fossil fuel imports.

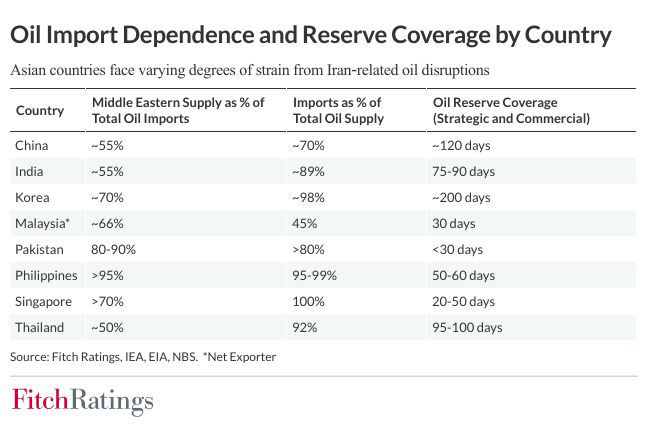

The impact would be uneven across the region. Large net fossil-fuel importers, such as India, Korea, Pakistan, the Philippines, the Maldives, and Thailand, would face the sharpest deterioration in external balances and real incomes if energy prices rise and shipping disruptions persist. Net energy exporters such as Australia and Malaysia could see a partial offset from higher hydrocarbon export receipts. However, Fitch does not expect any APAC sovereign credit profiles to benefit overall, given broader inflation-growth trade-offs and associated policy pressures.

Fiscal policy is likely to do most of the stabilization work in Asia, in line with government responses to the shocks of recent years, but buffers have thinned. Some jurisdictions have large fiscal cushions, including Singapore and Macao, yet public finances have weakened across many APAC sovereigns since the Covid-19 pandemic. The median government debt/GDP ratio is 50% in 2026, up from 49.5% in 2025 and 37.8% in 2019, and over 70% of sovereigns still run fiscal deficits above 2019 levels. Wider fuel, electricity, or fertilizer support would slow consolidation and could increase contingent liabilities where state-owned energy and utility companies absorb losses.

Beyond energy, credit profiles could weaken through other channels including exchange-rate depreciation, tighter financing conditions, and shifts in remittances and capital flows. External buffers will remain a key differentiator. Many APAC sovereigns hold significant foreign reserves and have resilient external financing structures, while some frontier markets face large refinancing needs and greater sensitivity to risk sentiment.

Supply-side disruption risks widen the shock beyond crude and liquefied natural gas. Shipping frictions and feedstock constraints are already spilling into industrial supply chains, with some Asian petrochemical producers declaring force majeure and cutting operating rates. This could worsen inflation expectations.

Governments are also beginning to use administrative measures to dampen demand and preserve supplies, such as reduced workdays and remote work to curb transport fuel demand. These steps may ease near-term demand pressures, but they also signal the risk that a longer disruption forces broader intervention, curtailing economic activity.

Fitch expects China to maintain restrictions on phosphate fertilizer exports into midyear, tightening supplies across the region. The Gulf’s central role in global fertilizer markets similarly raises the risk that higher natural gas prices and trade disruptions could push fertilizer costs up, feeding through into food prices and increasing subsidy burdens in countries with large support schemes. If fertilizer availability declines, crop nutrition could suffer, worsening yields and raising food security risks, particularly in frontier emerging markets with low incomes and limited fiscal buffers. Higher cost of living increases the risk of social tensions and protests.

The post APAC Sovereigns Face Greater Downside from a Prolonged Iran Conflict appeared first on Financial Chronicle Biz English | Sri Lanka Business News.