FINANCIAL CHRONICLE – The Central Bank of Sri Lanka is advised to cease its inflationary swaps and secure foreign reserves represented by excess liquidity, rather than temporarily absorbing this liquidity overnight to increase interest rates. A decline in short-term rates could lead to a swift credit recovery from Ditwah without formal rate cuts and deter speculative capital flows. Conversely, this approach could ensure lasting monetary stability.

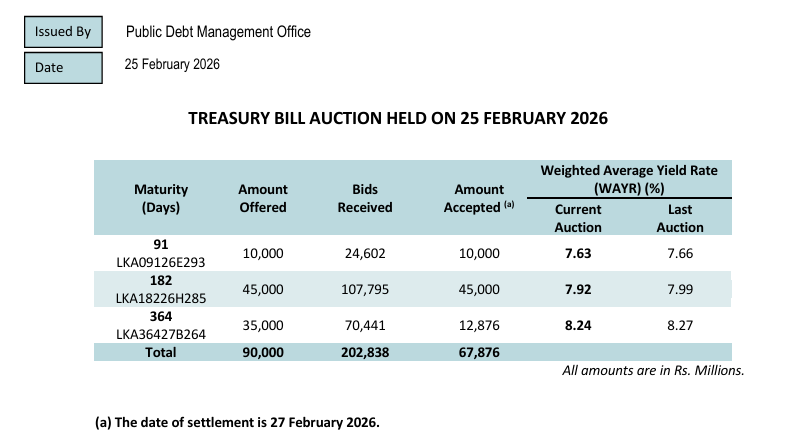

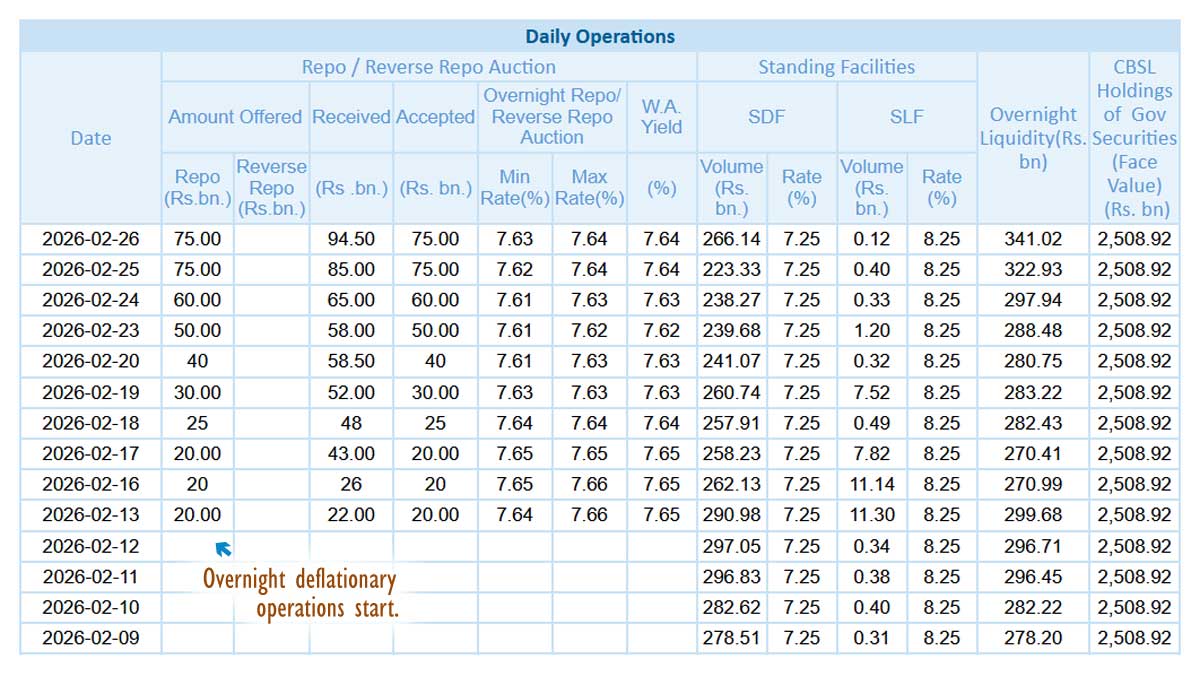

Last year, a combination of rising overnight rates and bill rates in December, driven by the Public Debt Management Office’s market-oriented auctions, contributed to some stability despite the discretionary exchange rate policy that denied convertibility. The central bank initiated deflationary open market operations on February 13, absorbing 20 billion rupees when overnight excess liquidity reached 297 billion rupees.

Slowdown

Some liquidity arose due to a slowdown in credit, which naturally reduces imports and reflects the current balance of payments status. This liquidity, stemming from dollar purchases by the central bank to prevent rupee appreciation, is a result of slow credit and is not immediately inflationary. It should lead to falling interest rates and a quicker credit recovery. There’s no need to cut rates when credit falls and liquidity builds up, as long as there’s a fixed exchange rate (a monetary rule).

Economic hardship and voter dissatisfaction with the democratically elected government stem from preventing the rupee from appreciating back towards 300 to the US dollar, a consequence of the denied convertibility in 2025. People must rely on the central bank’s discretion regarding the monetary unit’s value. A clean float without a reserve target would mean people wouldn’t have to depend on the central bank for economic stability.

Ditwah Aid and Rupee Depreciation

A portion of the liquidity originated from central bank purchases of Ditwah aid and remittances. If the central bank hadn’t excessively purchased dollars to accumulate reserves in December, the rupee could have returned to 300 to the US dollar, improving the government’s economic credibility and the people’s well-being. Ditwah funds, once spent by recipients, will prompt imports. Without the central bank defending the currency against liquidity created from monetizing the balance of payments surplus, the rupee will depreciate, as seen in 2005.

Democracy and Bad Money

The depreciation of the monetary unit isn’t directly caused by the government, except through the 5-7% inflation target the central bank convinced the elected government to accept. However, when the monetary unit’s value deteriorates, people blame the government. The political responsibility of an inflationist ‘independent’ central bank lies with the government in a democratic society, even though it’s not accountable. The government bears the consequences, as seen in the 2019-2022 administration’s experience with rate cuts targeting potential output. The subsequent government faced challenges in correcting policy.

Unfortunately, the operating framework hasn’t improved and has worsened with the single policy rate. Central bank independence is criticized as anti-democratic when the monetary authority is driven by inflationist ideology originating from the stimulus-oriented West. The discrepancy in governance is evident: strict fiscal rules for the elected government, but flexible non-rules for the unelected central bank.

Repo Operations

The central bank commenced overnight repo auctions, a deflationary measure, on February 13, 2026, when excess liquidity hit 297 billion rupees due to balance of payments developments and inflationary swaps. Overnight withdrawals have since increased to 75 billion rupees at 7.64%. Term operations began on February 25, at 7.74%.

While these deflationary operations are well-intentioned and benign, they won’t secure permanent reserves. The central bank should lock in reserves from Ditwah purchases and foreign bond acquisitions by terminating inflationary swaps. Unfortunately, parliament’s allowance of inflationary swaps has contributed to rupee depreciation through private bank reserves.

Conclusion

The repo operations, though well-intentioned, won’t help accumulate permanent reserves. Permanent forex reserves arise from sustained deflationary operations. Maintaining a single policy rate could encourage more hot money into rupee securities. Some East Asian nations eliminate the floor rate and deflationary term operations during credit slowdowns, allowing rates to fall faster and aiding credit recovery.

If Sri Lanka’s parliament can maintain a strong monetary unit, interest rates will eventually fall as domestic capital destruction ceases. The classical economic view that interest rates are a function of capital, not reserve money, should be considered. Sri Lanka cannot sustain a single policy rate, an IMF reserve target, and repay foreign debt simultaneously. Following practices of countries that avoid the International Monetary Fund or revert to classical economic rules after external crises may lead to sustainable growth and stability.