FINANCIAL CHRONICLE – W A Wijewardene, a former Deputy Governor of the Central Bank of Sri Lanka, has advocated for an inflation target of 2 percent, with a maximum ceiling of 3 percent. He believes that such a target would enable people to make informed long-term decisions regarding savings and investments.

Since September 2022, Sri Lanka’s central bank has provided remarkable stability to the economy through broadly deflationary policies, even though it missed its initial inflation target of 5-7 percent. However, some concerns remain about the potential depreciation of the currency if bank dollar assets are monetized without defending the rupee using ‘borrowed’ reserves.

According to Wijewardene, the country’s inflation rate is currently around 2 percent per annum, as indicated by both the Colombo Consumer Price Index and the National Consumer Price Index. “This is a favorable development as such low inflation encourages people to adopt a long-term economic perspective, fostering savings and investments,” Wijewardene noted in his column in Sri Lanka’s Daily FT newspaper. “A low inflation rate also contributes to exchange rate stability and results in lower interest rates, which are beneficial for long-term economic growth.”

He argued that it is inappropriate to criticize the central bank for missing an undesirable target while achieving favorable economic conditions. “Instead of reprimanding the Central Bank for failing to meet the target, which in itself is undesirable, the Central Bank and the Finance Minister should agree on a new monetary policy framework. This framework should mandate the Central Bank to achieve a 2 percent inflation target with a leeway of one percentage point either way. Such a target aligns with the country’s average productivity growth levels and is neutral on the welfare of the populace.”

Wijewardene pointed out that Sri Lanka’s productivity growth appears to be around 2.0 to 2.1 percent. He also referenced the historical context, noting that when the central bank was established, banks in what was then Ceylon were purchasing 20-year government bonds. The Federal Reserve’s yet-to-begin ‘rate cutting’ cycles led to deliberate credit cycles, causing wild rate fluctuations and routine ‘market to market’ losses. Before these fluctuations, spikes in interest rates were rare and mainly limited to wartime, reducing the fear of long-term investments.

In 2017, during World War I and shortly after the Fed’s creation but before its open market operations began, civilians purchased 30-year Liberty Bonds at 3.5 percent. The Fed’s open market operations, initiated in April 1923 to implement deflationary policy, eventually led to a credit bubble and the Great Depression in the following decade.

Prior to the policy rate, when private central banks were tightly bound by the gold standard, the British government issued ‘perpetuals’ (bonds with no maturity date), which could be purchased without the risk of steep mark-to-market losses.

Analysts have called for a 2 percent inflation ceiling, which would further limit the central bank’s ability to depreciate the currency and potentially incite social unrest. Some have also advocated for an exchange rate target. Unlike an inflation target that can be manipulated by altering the base after currency crises, exchange rates are more transparent, and econometrics cannot be used to artificially lower index inflation.

Many Sri Lankans who previously relied on three-wheelers for transportation are now using buses, and those who opted for private healthcare are turning to state hospitals following the last currency collapse. This shift is attributed to potential output targeting and will likely be reflected in a re-basing based on current consumption patterns, analysts suggest.

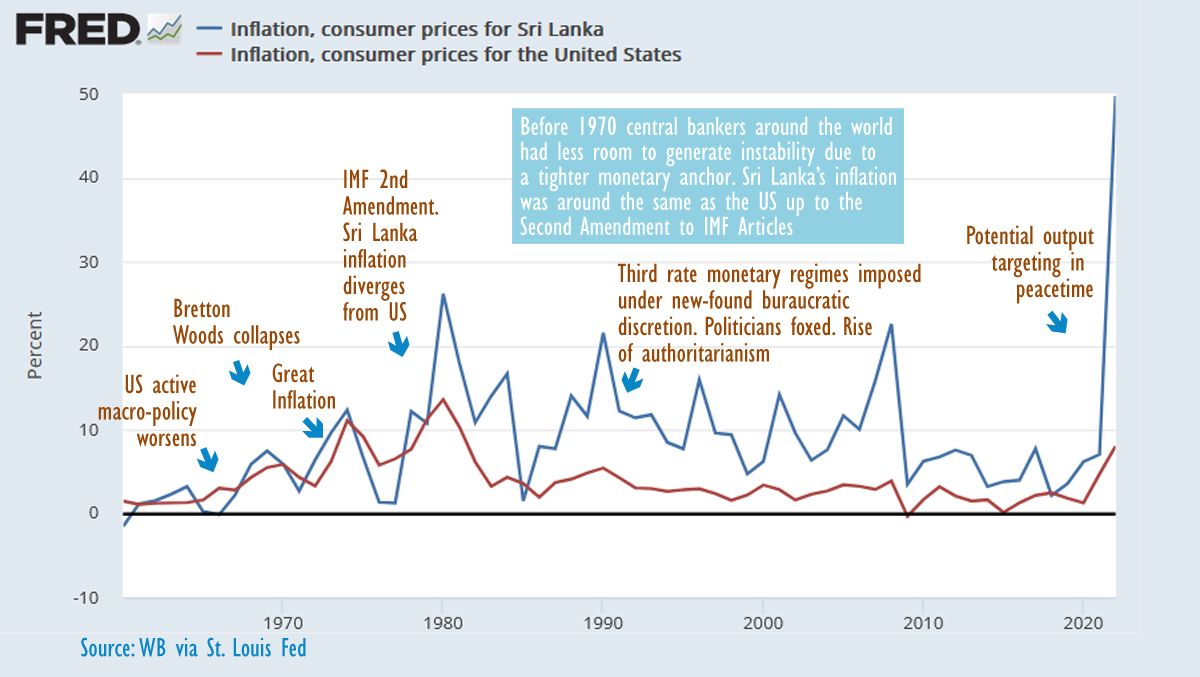

Sri Lanka’s inflation began to deviate from that of the US in the 1980s, following the IMF’s second amendment to its articles, which coincided with the rupee’s depreciation. The recent high inflation emerged after the exchange rate was used as the primary defense, which critics argue allows the central bank to avoid accountability for flaws in its operational framework, such as implementing inflation-targeting frameworks without a floating exchange rate or sterilizing reserve sales with inflationary open market operations.

(Colombo/Mar04/2026)