The recent US-Israeli attacks on Iran and the subsequent retaliation from Iran might pose additional challenges for certain emerging market sovereigns, including Sri Lanka. According to Fitch Ratings, these challenges could manifest through various channels such as energy imports, remittances, fiscal subsidies, exchange rates, and access to international finance.

Fitch Ratings highlighted that “oil and gas imports are the most direct channel for contagion from the conflict, given its effect on global energy prices.” This statement came before oil prices surged over 20 percent, surpassing $100 a barrel on Monday. The agency noted that markets with already strained financing capacities, such as Pakistan, or those with significant current account deficits, are most vulnerable to the rising import costs.

Sri Lanka’s economy is currently recovering from a default in 2022 and is in the process of stabilization with support from the International Monetary Fund (IMF) and ongoing debt restructuring efforts.

The full statement from Fitch Ratings elaborates on the risks posed by the Iran conflict to emerging market sovereigns. It suggests that hydrocarbon exporters might experience positive effects, while the effective closure of the Strait of Hormuz, if lasting less than a month and without significant damage to the region’s oil production infrastructure, should contain risks to emerging market ratings. However, a longer closure or sustained effects could have a more substantial impact.

For many small emerging markets, net fossil fuel imports constitute a large portion of GDP. Among the larger economies, these imports account for 3% or more of GDP in countries like Chile, Egypt, India, Morocco, Pakistan, the Philippines, Thailand, and Ukraine.

Fitch anticipated a significant current account deficit in Ukraine (15.4%) in December 2025, with moderate deficits expected in the Philippines (3.4%) and Egypt (3.0%). Prolonged high energy prices could exacerbate external strains for these sovereigns, particularly if other stresses, such as disruption to remittances, emerge.

Where sovereigns are running current account surpluses, like Thailand, external finance risks will be limited. However, prolonged higher energy prices could also increase fiscal strains for governments with subsidy regimes aimed at shielding consumers or those that implement similar measures in response to higher energy prices.

A more sustained disruption to global energy supplies from the Gulf than expected could negatively impact global investor sentiment. This scenario could strengthen the US dollar and weaken the market for debt issuance, particularly for highly speculative-grade issuers. Furthermore, higher energy prices might put upward pressure on inflation, influencing monetary policy decisions globally.

These factors are likely to increase the cost of servicing and refinancing debt for emerging market sovereigns. However, many countries frontloaded a significant portion of their planned foreign-currency issuance for the year in January-February, thereby enhancing their flexibility against temporary market volatility.

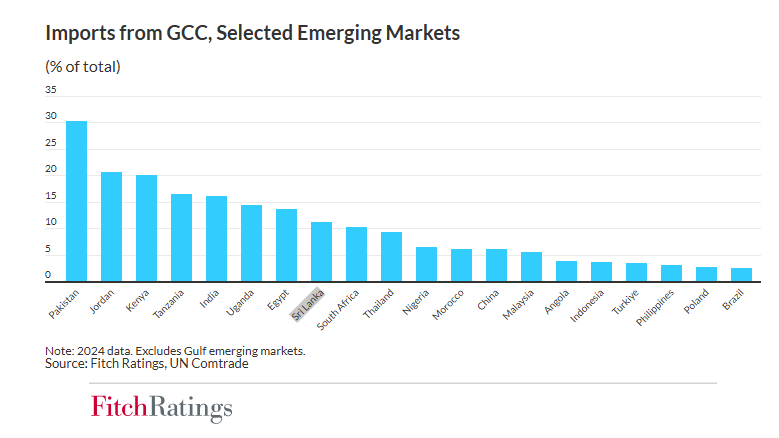

Weaker non-oil activity in Gulf Cooperation Council (GCC) states, due to damage to logistics and tourism sectors, will adversely affect countries reliant on exports to the affected region or remittance flows. Egypt and Jordan are particularly exposed to risks from tourism and remittance disruptions, while remittances from the GCC region are crucial for South Asian countries. Additionally, countries with high import concentration from the GCC could face supply chain disruptions, potentially affecting output and prices.

The conflict’s effects on other commodity markets could also be significant for some emerging markets. The Gulf region is an important producer of aluminum, and its role in producing inputs for the fertilizer industry might have medium-term repercussions if it affects global food production and inflation.

There are also unique scenarios through which the crisis could impact certain countries. Azerbaijan, Iraq, and Turkey might be affected if instability in Iran leads to a major refugee outflow.

For emerging market net hydrocarbon exporters outside the Gulf, such as Angola, Argentina, Azerbaijan, Brazil, Colombia, Ecuador, Gabon, Kazakhstan, Nigeria, and the Republic of Congo, a prolonged period of higher energy prices could result in an export and fiscal windfall. Fitch Ratings will consider the durability of improvements in external and public finance positions in their rating assessments.