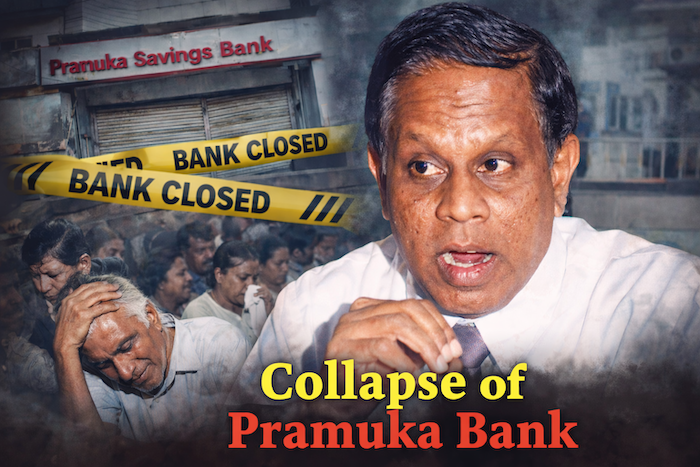

he collapse of Pramuka Savings and Development Bank remains one of the most defining moments in Sri Lanka’s modern financial history. It was not merely the failure of a bank, but the exposure of deep-rooted weaknesses in corporate governance, risk management, and regulatory oversight. What makes Pramuka’s story even more extraordinary is that it did not end with liquidation. Years after its failure, the institution was resurrected under a new name and structure by the Central Bank—leaving behind a legacy that continues to provoke debate about accountability, restitution, and trust.

Pramuka Bank commenced operations on 21 July 1997, founded by Rohan Perera, a banker with more than thirty years of experience locally and internationally. Perera was widely known as the former founder and chief executive of Seylan Bank, which had expanded rapidly under his leadership. However, his departure from Seylan Bank in 1996, amid allegations of foreign exchange irregularities, cast an early shadow over his next venture. Despite these concerns, Perera went on to establish Pramuka Bank, securing a licence from the Central Bank of Sri Lanka—not as a commercial bank, as he had sought, but as a Savings and Development Bank.

From the outset, Pramuka’s governance structure was deeply flawed. Perera held the positions of Chairman, Chief Executive Officer, and Managing Director simultaneously, concentrating extraordinary power in one individual. The board of directors—comprising figures such as Udaya Nanayakkara, Camillus Perera, Lasanga Jinadasa, J.A.D. Lanerolle, Dr. C.W.P. Canagaratna, A.H.A. Mendis, and Lucien Fernando—included respected personalities from business and public life, but most lacked the banking and financial expertise required to oversee a deposit-taking institution. As a result, Perera’s decisions went largely unchallenged, and the board failed in its fundamental duty of oversight.

Operationally, Pramuka was burdened by structural and regulatory constraints. The bank was denied parate execution rights, which meant it could not swiftly recover defaulted loans by selling mortgaged properties. It was also restricted to operating a single branch, severely limiting its ability to build a stable deposit base. While these factors contributed to stress, they were not the root cause of failure. The decisive damage came from reckless management and the absence of sound internal controls.

Pramuka’s lending practices were deeply irresponsible. Credit was extended without proper appraisal, documentation was often incomplete or misleading, and exposure limits imposed by the Central Bank were repeatedly breached. Loans were approved to politically exposed individuals and financially unstable companies, sometimes in direct violation of the bank’s own policies. When borrowers defaulted, new loans were issued to mask non-performing advances, creating an illusion of asset quality. Internally, risk management systems existed largely on paper and were routinely ignored.

As losses mounted, transparency was abandoned. Financial statements were manipulated through aggressive accounting practices, including changes in revenue recognition, allowing operating losses to be converted into reported profits. Loan portfolios were reclassified to conceal bad debts, and material disclosures were withheld from stakeholders. Auditors raised concerns, but vital information was concealed from them. Pramuka had no effective audit committee, no risk oversight, and no governance culture to restrain misconduct.

The ethical collapse went further. Employees’ Provident Fund contributions were diverted into an unapproved internal fund and reinvested in Pramuka’s own securities, exposing around 160 employees’ retirement savings to the bank’s failure. Fraudulent property transactions and violations of banking, labour, and criminal laws compounded the crisis.

By October 2002, Pramuka’s financial condition was beyond repair. Non-performing assets had risen to nearly 80 percent of the loan book, bad debts exceeded Rs. 2.2 billion, and the bank’s net worth had turned deeply negative. When depositors lost confidence, a bank run followed. Pramuka was unable to meet withdrawal demands. The Central Bank intervened, suspending operations, and in August 2004 the Monetary Board cancelled Pramuka’s banking licence and ordered its liquidation—the first time a licensed bank had been shut down in Sri Lanka.

The human cost was devastating. Thousands of depositors lost life savings. There were reports of suicides, heart attacks, and widespread psychological trauma among those affected. Public confidence in the banking system was shaken at a national level. As the crisis unfolded, Rohan Perera fled the country, leaving behind unresolved questions of responsibility and accountability.

Yet Pramuka’s story did not end with liquidation. In the years that followed, the Central Bank and the Government sought ways to recover assets and provide some measure of relief to depositors. The banking licence and institutional shell of Pramuka were revived under a new entity, Sri Lanka Savings Bank Ltd., which took over the management of Pramuka’s remaining assets. This was not a continuation of the failed bank, nor did it inherit its liabilities in full. Instead, it functioned as a recovery vehicle, tasked with realising assets and making partial repayments to affected depositors.

By 2015, Sri Lanka Savings Bank announced that over 8,000 former Pramuka depositors would receive payments amounting to approximately Rs. 240 million, funded through recovered assets and operational income. While these payments offered some relief, they fell far short of restoring what many depositors had lost. For many, the resurrection of the bank’s licence without full restitution felt like institutional closure without justice.

The collapse of Pramuka Bank forced sweeping reforms. Capital requirements for banks were raised, corporate governance rules were made mandatory, director duties were strengthened under the Companies Act, and regulatory oversight of auditors and financial institutions was tightened. These reforms were designed to ensure that no bank could again fail so spectacularly through unchecked power and unethical conduct.

Pramuka’s legacy is therefore complex. It is a story of ambition unrestrained by accountability, of governance failure amplified by regulatory gaps, and of human suffering that cannot be measured solely in financial terms. Its resurrection as Sri Lanka Savings Bank represents an attempt at institutional repair, but it does not erase the scars left on depositors or the lessons written into Sri Lanka’s financial history.

In banking, trust is the ultimate asset. Pramuka lost it.

And no resurrection can fully restore what was broken when that trust collapsed