Sri Lanka’s insurance industry is entering a strong recovery phase, supported by rising economic stability, higher financial literacy, and renewed demand for protection-based products. According to industry data, the sector—comprising both Life and General insurance—has demonstrated broad-based growth, with Life insurance continuing to lead the industry’s expansion.

Life insurance now represents 57% of the total market, driven by increasing interest in retirement planning, health-related products, and long-term savings. Gross Written Premiums (GWP) in the Life segment grew by 20.5% in 2024, marking its strongest expansion in five years, while the momentum carried into 9M2025 with a robust 25% YoY growth. Total assets in the Life sector rose to LKR 921 billion in 2024, reflecting a 12.6% increase and underscoring strengthening policyholder funds and investment portfolios.

General insurance, representing 43% of the market, has also shown resilience, supported by recovering consumption and improving business confidence. Motor, health, fire, and marine segments remain core contributors, with motor insurance particularly benefiting from an uptick in vehicle imports and economic activity.

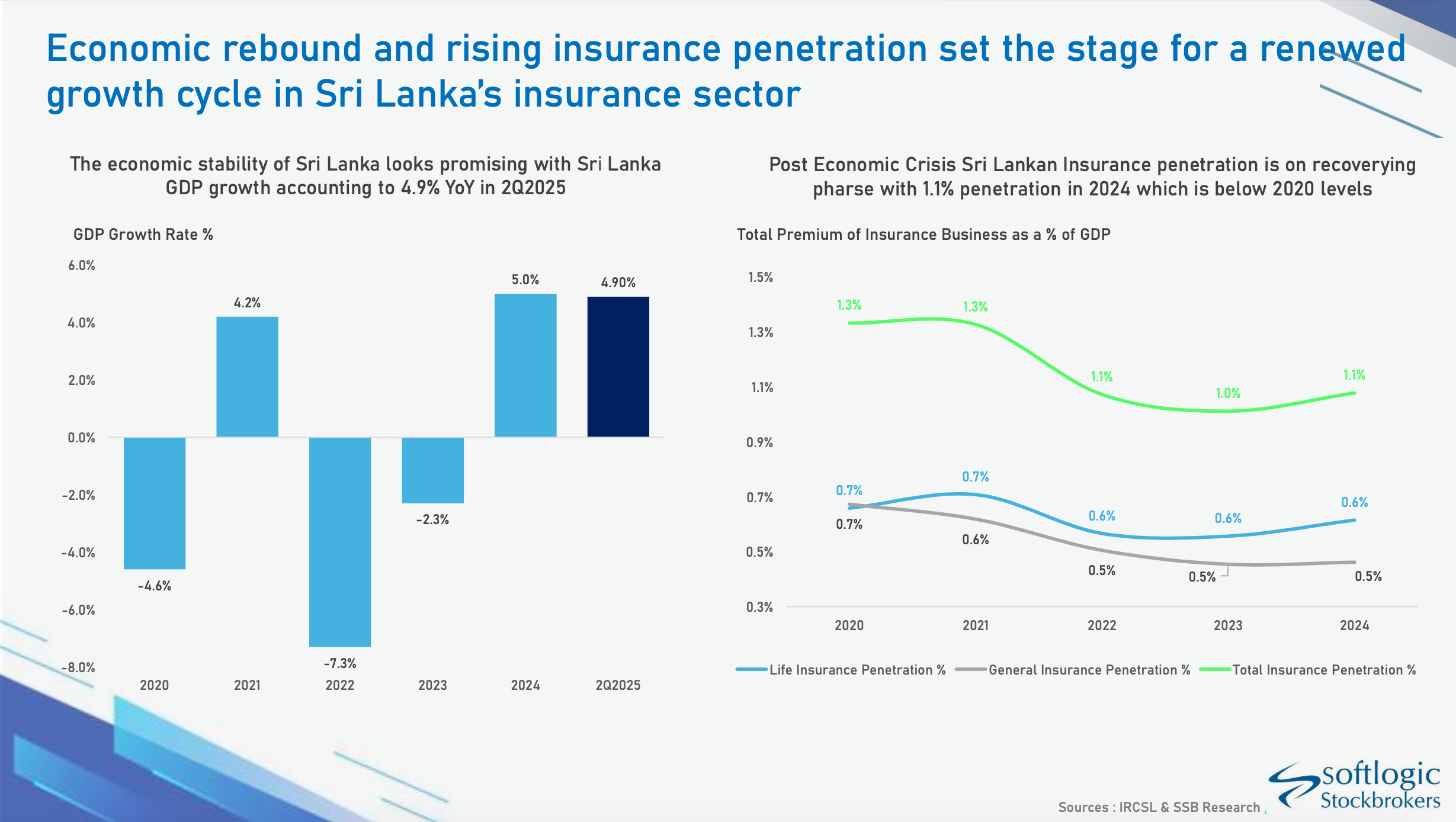

Despite the positive trajectory, Sri Lanka’s insurance penetration—at 1.1% of GDP in 2024—remains below pre-crisis levels and significantly lower than regional peers. Premium income per capita stands at approximately USD 54, indicating a substantial untapped market with long-term growth potential.

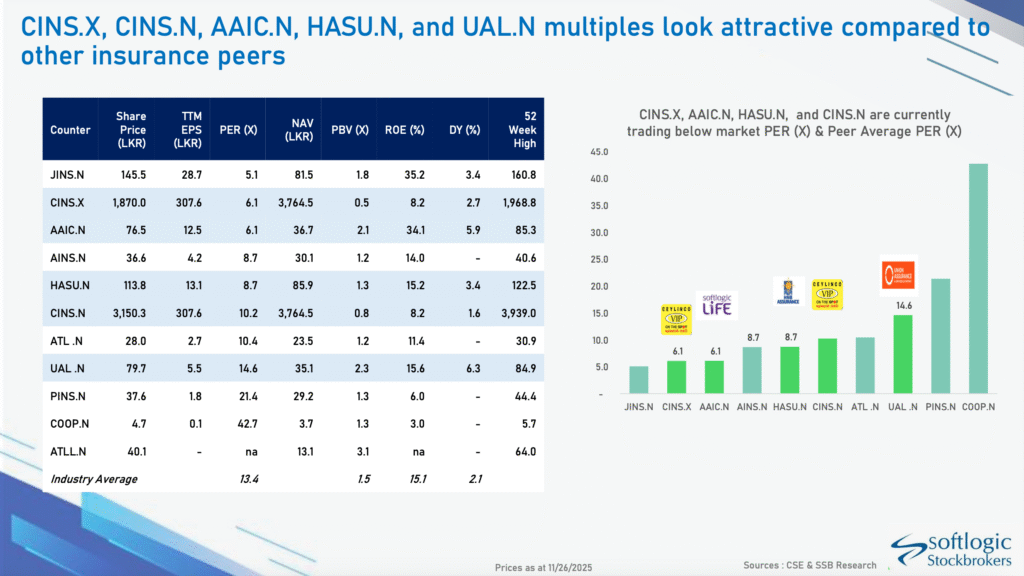

Sector-wise performance highlights Ceylinco Life’s continued market leadership with a 20% share of total GWP as of 9M2025, followed by Softlogic Life at 17%—a position further strengthened by its recent acquisition of Allianz Life. HNB Assurance and Union Assurance also reported solid premium expansions, driven by strong Life policy renewals and diversified product offerings.

Listed insurance companies posted mixed profitability, with Ceylinco (CINS) recording the highest equity holders’ profit of LKR 5.4 billion for 9M2025, while Softlogic Life delivered strong GWP growth and the highest new policy additions among peers. Union Assurance and HNB Assurance recorded healthy premium growth, though profitability was affected by higher reserve requirements and rising claims.

Looking ahead, industry analysts expect sustained growth as economic conditions stabilize, interest rates moderate, and insurance awareness deepens. Rising demand for health and protection-based Life products, digital distribution expansion, and product innovation are expected to fuel sector momentum. While higher claims and actuarial reserve pressures may weigh on short-term profitability, the medium-term outlook remains strongly positive, with insurers well-positioned to capture long-term structural growth in one of the region’s lowest-penetrated insurance markets.